Expenses normally have debit balances that are increased with a debit entry. Since expenses are usually increasing, think “debit” when expenses are incurred. The petty cash account should be reconciled and replenished every month to ensure the account is balanced and any variances are accounted for. The accountant should write a check made out to “Petty Cash” for the amount of expenses paid for with the petty cash that month to bring the account back up to the original amount.

What is the Journal Entry to Record Sales Total with a Cash Overage?

- This essentially transfers the funds from the main cash account to the petty cash account.

- Since the petty cash account is an imprest account, this balance will never change and will remain on the balance sheet at $75, unless management elects to change the petty cash balance.

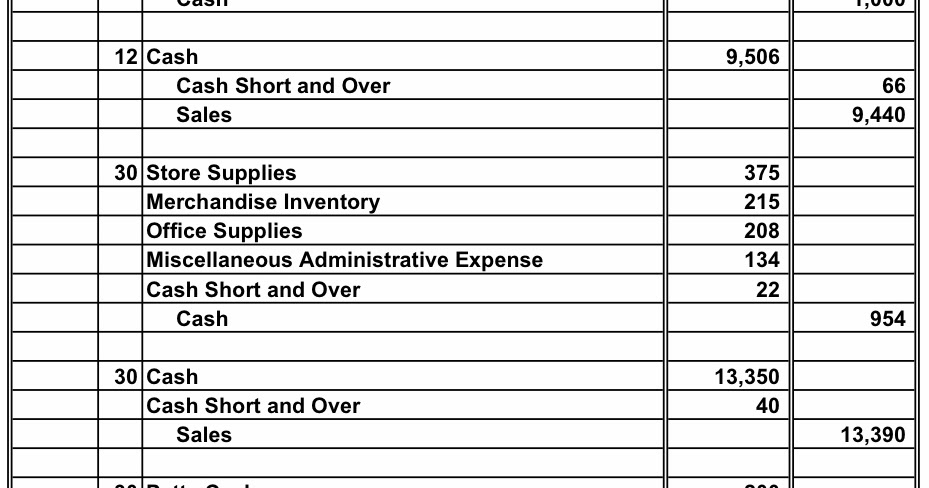

- In this case, we can make the journal entry to record the cash overage by debiting the cash account and crediting the cash over and short account and the sales revenue account.

- This reduces the balance in the petty cash account to reflect the expenditure.

If you need help getting a petty cash log started, look up some free petty cash log templates to do some of the work for you. While petty cash is a relatively small amount of money, it can be easily stolen or abused if you don’t handle it right. Since 2016, Stenn has powered over $20 billion in financed assets, supported by trusted partners, including Citi Bank, HSBC, and Natixis. Our team of experts specializes in generating agile, tailored financing solutions that help you do business on your terms. This example illustrates how a small fund can facilitate quick, necessary purchases throughout the day without disrupting workflow or requiring complex approval processes. As a business grows, managing petty cash across multiple locations or departments can become increasingly complex.

How to Figure Shorts & Over Entries in Accounting

Another strategy is ensuring that petty cash disbursements are made for legitimate purposes, with proper documentation and approval. It is essential to maintain accurate records, as this makes it easier to trace any discrepancies. Proper documentation, like receipts and vouchers, should be required for all disbursements to create a permanent record and establish transparency. To maintain accurate records, be sure to collect original receipts for each expenditure. Receipts should be attached to the corresponding petty cash voucher and filed for future review and reconciliation. Assume the same situation except that I receive $94 instead of $96 for the sale.

Accounting

Also, the debit of cash over and short represents the loss, e.g. a few dollars, due to the cash being less than the amount it is supposed to be when comparing the sales records. Reconciliation of a petty cash account involves comparing the remaining cash balance with the total recorded transactions in the petty cash log. Discrepancies should be investigated, and corrective actions should be taken if needed. This reconciliation process helps maintain the accuracy and integrity of the petty cash system and ensures that the fund is used appropriately. As we have discussed, one of the hardest assets to control within any organization is cash. One way to control cash is for an organization to require that all payments be made by check.

Policies should be established regarding appropriate expenditures that can be paid from petty cash. When a disbursement is made from the fund, a receipt should be placed in the petty the petty cash account cash short and over is a permanent account. cash box. At any point in time, the receipts plus the remaining cash should equal the balance of the petty cash fund (i.e., the amount of cash originally placed in the fund).

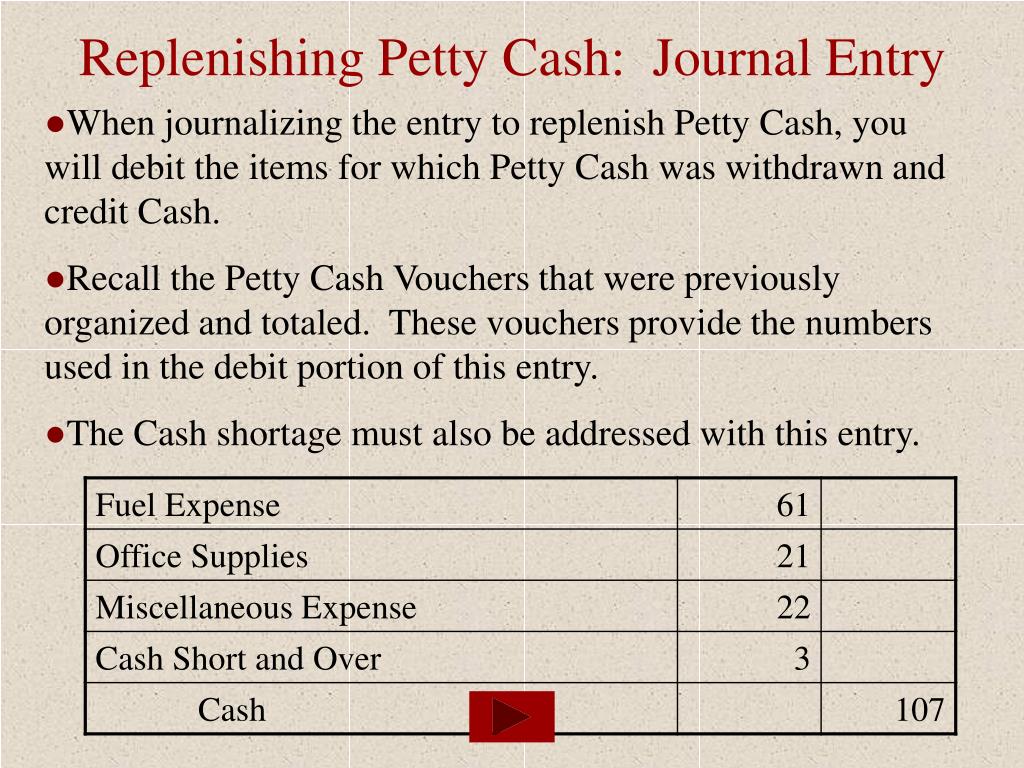

This journal entry, in essence, subdivides the petty cash portion of available funds into a separate account. After calculation, even though the total petty cash expenses are only $82 ($45+$25+$12), we need to replenish $85 ($100-$15) as we have only $15 cash on hand left. Likewise, the $3 difference is the cash shortage that we need to recognize as a small loss. Petty cash reporting is an essential process in maintaining an accurate and up-to-date record of a company’s financial transactions. It involves keeping track of all deposits and withdrawals from the petty cash fund and ensuring that each transaction is accounted for. A designated employee, known as the custodian, is responsible for managing and safeguarding this fund.

If the remaining balance is more than what it should be, there is an overage. Although there can be minor variances, when unbalanced, the source of the discrepancy should be identified and corrected. Instead of processing numerous small transactions individually, businesses can record petty cash replenishments as a single entry, streamlining bookkeeping. In the world of business finance, petty cash might seem like a small change, but it can make a big difference in your day-to-day operations. This often-overlooked financial tool is the unsung hero of smooth-running businesses everywhere.

The term cash over and short refers to an expense account that is used to report overages and shortages to an imprest account such as petty cash. The cash over and short account is used to record the difference between the expected cash balance and the actual cash balance in the imprest account. Whenever cash is received, the asset account Cash is debited and another account will need to be credited. Since the service was performed at the same time as the cash was received, the revenue account Service Revenues is credited, thus increasing its account balance.

The sum of the cash and receipts will differ from the correct Petty Cash balance. This might be the result of simple mistakes, such as math errors in making change, or perhaps someone failed to provide a receipt for an appropriate expenditure. Whatever the cause, the available cash must be brought back to the appropriate level. For example, assuming that we have a cash overage of $10 instead in example 1 above, as a result of having actual cash on hand of $2,800 which is more than the cash receipts of $2,790. Thus, this account serves primarily as a detective control—an accounting term for a type of internal control that aims to find problems, including any instances of fraud, within a company’s processes.

It’s “other revenue” for you, not a normal source of revenue like your paycheck. Determining the right amount of petty cash for your business is crucial for maintaining efficiency without exposing yourself to unnecessary risk. Processing small transactions through a company’s main accounting system can be time-consuming and costly.

In this journal entry, the credit of the cash account is to refill the petty cash fund to its full established petty fund. At the same time, it also represents the cash outflow from the company as a result of petty cash expenses during the period. When petty cash is used for expenses, it is essential to record the transactions in the general ledger. For example, if petty cash is used for postage expenses, a journal entry would be made to debit the postage expense account and credit the petty cash account. This reduces the balance in the petty cash account to reflect the expenditure.